Silico Manganese Production. Ferroalloys Industry

The global market for Silicomanganese is expected to grow at a CAGR of roughly 6.0% over the next five years.

Silico manganese is an alloy with 60% to 68% manganese, 14% to 21% silicon, and 5% to 2.5% carbon. It is produced by smelting of slag from high-carbon Ferro Manganese or of Manganese ore with coke and a quartz flux in a submerged electric arc furnace. The process requires power consumption of about 3,800 to 4,800 kilowatt-hours per tonne.

Silico Manganese is an essential component as an ingredient in the process of manufacturing various grades of steels. Silico Manganese, High Carbon Ferro Manganese, Medium Carbon Ferro Manganese, is covered under routine production planning. In addition the existing EAF has also successfully produced Pig Iron on market demand.

Silico Manganese is one of the essential alloy that contains both the elements of manganese and silicon. As well, this range is manufactured by heating a combination of silicon dioxide, manganese oxide and iron oxide along with carbon at the vendor’s end. Silico manganese is usually used as deoxidizers and desulfurizers.

Market Outlook

The worldwide market for Silico Manganese is expected to grow at a CAGR of roughly 6.0% over the next five years, will reach 19400 million US$ in 2024, from 14500 million US$ in 2019.

Driving factors responsible for the growth of Silico Manganese Market includes rising urbanization that demands commercial products such as utensils and other domestic products. Other major factors such as demand for steel, dairy equipment, hand railings and other commercial items also contribute to the growth of Silico Manganese Industry. However, varying availability of silico manganese in certain geographical areas raises the transportation and logistics costs wherein this factor slightly hampers the market growth.

Global Silico Manganese Market is expected to gain a significant CAGR in the forthcoming period. Silicon and Manganese are crucial components in steel manufacturing units as deoxidants, desulphurizers and alloying elements. The primary deoxidizer is Silicon. Manganese serves as a deoxidizer in small doses than Silicon but it enhances the effectiveness since stable manganese silicates are mixed with aluminates. It also caters to the steel industry as desulphurizer. Manganese serves as an alloying element in all types of steel.

The key players in the Silico Manganese Market include Erdos Group, Sheng Yan Group, PJSC Nikopol, Henan Xibao Metallurgy Materials Group, Ningxia Jiyuan Metallurgical Group, Bisheng Mining, Jinneng Group, Guangxi Ferroalloy, Eurasian Resources Group, Fengzhen Fengyu Company, Glencore, TATA, and Zaporozhye.

Ferroalloys Market

Owing to the lack of a viable alternative that can meet the diverse applications, the future of the global ferroalloys market is healthy, expanding at an estimated CAGR of 5.9% during the forecast period of 2017 to 2025. The prosperity of the building and construction industry in a number of emerging economies is another key driver of the global ferroalloys market, wherein the development of lightweight and high strength steel grades is expected to open new opportunities.

On the other hand, stringent governmental regulations pertaining to the environment and high operational costs are two glaring restraints over the global ferroalloys market. Ferroalloy Market size was estimated over USD 45 billion in 2017 and the industry will grow by a CAGR of more than 5.5% up to 2025.

Rising demand for steels in end user industries such as construction, shipbuilding, automotive and several other sectors is one of the major drivers for ferroalloy market. The product has main applications in manufacturing variety of steels such as stainless steel, alloy steel, carbon steel, etc. Presence of iron ore in abundance across the globe along with intensifying demand for various types of steel grades owing to lack of feasible substitutes will give an up thrust to ferroalloy market in near future. Global crude steel production was about 1.6 billion tons in 2017, and showed a growth rate of around 5.3% in comparison to last year. The emerging nations such as China and India hold significant shares in this as the prime demand centers for steel.

Some of the major automobile manufacturers are present in these countries catering to the increasing demand from the local customers. Expanding population along with improving standard of living gives boost to construction sector as well. Recent initiatives taken by governments in Asia Pacific region to boost manufacturing sector will also catapult ferroalloy demand over forecast time period.

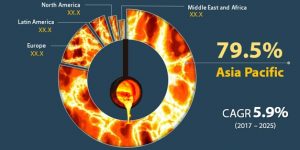

Global Ferroalloys Market Share (%), By Region (2017)

Based on type, the global ferroalloys market has been segmented into two major categories, viz. bulk ferroalloys and noble ferroalloys. Bulk ferroalloys is further sub-segmented into ferrosilicon, ferromanganese, ferrochromium, ferro-silico-manganese, and ferro-silico-chromium. Manganese plays an essential part in the production of most varieties of steels and it is also one of the most important element in the production of cast iron. Most of the noble ferroalloys are made from rare earth minerals and are expensive to produce as compared to bulk ferroalloys. Most of the noble alloys are made from adding chromium, tungsten, nickel, boron, vanadium, niobium, titanium, cobalt, copper, molybdenum, phosphorus, and zirconium. These rare earth metals helps in contributing special properties and character to the various alloy steels and cast irons.

India produces 3.5 million tonne (mt) of ferro alloys and consumes around 2.3 mt. The country exported 1.3 mt of ferro alloys, earning a foreign exchange of around Rs 8,900 crore. India’s production of around 3.5 mt of ferro alloys consists of one million tonne of ferro chrome (FeCr) and 2.5 mt of manganese alloys.

Ferroalloy production in the organized sector started in the mid-sixties of the last century. Initially, ferroalloy units came up in the states of Andhra Pradesh, Karnataka, Odisha and Maharashtra mainly due to Availability and proximity of raw material sources.

See more