Production of Low Carbon Ferro Chrome. Opportunities in Ferrochrome, Ferroalloys Industry

Low Carbon Ferro Chrome offered comprise ferrochrome ortant chromium ore. It works as alloy of chromium & iron and comprises between 50% and 70% chromium content and provides usage as important iron niobium alloy with niobium content of 60-70%. Further, it is also used as main source for niobium alloying of HSLA steel.

Low carbon Ferro-alloys are used for DE oxidation of steels as well as for introduction of the alloying elements in the steel during the steel making process. By addition of specialty ferroalloys during the production of steel, the properties (mechanical, joining etc.) of the steels are upgraded.

- Provides for wide usage in foundry and steel industry

- Made available with optimum chemical and physical properties

- Finding usage during steel production for correcting chrome percentage without causing undesirable variation in carbon/trace element percentage

- Also suitable as low cost alternative to metallic chrome for use in super alloys as well as other special melting

It is a Ferro alloy with high content of manganese. It gives strength to steel and is used in making of high tension steel. Low carbon Ferro manganese is widely used in the manufacturing of tool steels, alloys steel & structural steels. Its property causes it to have a high affinity with sulphur in the steel and on combining produces Manganese Supplied (MN’s) which floats up to the metal surface. Low Carbon Ferro Manganese is used as a de-oxidizer and hence finds its usage in the manufacture of 18-8 Austenitic nonmagnetic stainless steel.

Market Outlook

Low Ferro chrome is an alloy of chromium & iron, it encloses 50% – 70% of chromium by weight. A ferrochrome manufacturing process is mostly conducted by the carbothermic reduction of chromite in an electric submerged arc furnace (SAF). In modern industries, one of the main ferrochrome uses is to produce stainless steel, as it imparts strength and durability. The global low ferrochrome market is growing significantly in the developing countries that are China, India, South Africa, Brazil and Indonesia, because of their large demand of stainless steel and other alloy steel in the construction industry.

Low Ferrochrome market is increasing consolidated with several major ferrochrome producers leading the ferrochrome production globally. Meanwhile, the high production and rich reserves of metallurgical chromite and other raw materials in South Africa, Zimbabwe, and Kazakhstan are also fuelling the ferrochrome market globally. At last, the increasing use of stainless steel around the world for various end-user industries, such as construction and automobile, is anticipated to be one of the major factors driving the global ferrochrome market forward throughout the forecast period.

Charge chrome and high carbon segment are expected to hold the largest ferrochrome market share during the forecast period. Charge chrome and high carbon ferrochrome provide boosted hardenability, temperature stability and corrosion resistance of stainless steel. The huge majority of FeCr produced is charge chrome from South Africa. With high carbon being the largest segment sectors of low carbon and intermediate carbon material.

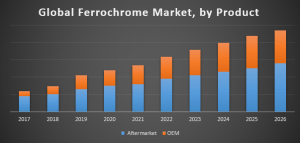

Global Ferrochrome Market, By Product

Stainless steel is dominating the global ferrochrome market. The use of chromium-grade and chromium manganese grade stainless steel in the construction and transportation industries is anticipated to have a huge positive impact on ferrochrome market. Region-wise, the Asia Pacific region is presently the largest ferrochrome consumer, Europe and North America, owing to the fact that the Asia Pacific accounts for more than 70% of the global stainless steel production. The growing demand for stainless steel from the construction, transportation, and metallurgical industries in the Asia Pacific will be the main driver of the ferrochrome market growth over the upcoming year.

The slag processing plants help in the easy recovery of ferrochrome metal. The ferrochrome slag can be used as aggregate in construction industry. The growing environmental concerns about the proper ferrochrome waste slag is expected to foster market growth. The worldwide market for low Ferrochrome is expected to grow at a CAGR of roughly 10.1% over the next five years, will reach 21100 million US$ in 2024, from 11900 million US$ in 2019.

Key players

Glencore-Merafe, Eurasian Resources Group, Samancor Chrome, Hernic Ferrochrome, IFM, FACOR, Mintal Group, Tata Steel, IMFA, Shanxi Jiang County Minmetal, Jilin Ferro Alloys, Ehui Group, Outokumpu, Samancor Chrome, Yildirim Group of Companies, Afarak, ENRC, GLENCORE, Tata Steel, Samancor, Hernic Ferrochrome, Fondel Corporation, Tharisa, Westbrook Resources, ICT Group, Sinosteel, Rohit Ferro Tech, Tennant Metallurgical Group, Ferro Alloys Corporation, ZIMASCO, ZimAlloys, Maranatha Ferrochrome, Oliken Ferroalloys, Vargon Alloys, Indsil, Harsco, Anjaney Ferro Alloys Ltd, Bansal Ferrous Ltd, Ferro Alloys Corpn. Ltd, Impex Ferro Tech Ltd, Jagat Alloys Pvt. Ltd, Acme Ferro Alloys Pvt. Ltd., Balasore Alloys Ltd, Indian Metals & Alloys Ltd, Indsil Hydro Power & Manganese Ltd.